"Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens..."

- John Maynard Keynes

"The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing."

- Jean-Baptiste Colbert

"If you get up early, work late, and pay your taxes, you will get ahead... if you strike oil"- J. Paul Getty

The phrase "inflation tax" is a flippant jab at government (by nerds, admittedly), but one that I think most people intuitively understand. The idea is simple. When the government prints money (or runs enormous deficits, which more or less amounts to the same thing), the purchasing power of your dollars declines. That is a tax on your savings, even if no one sends you a bill.

What most people do not realize is that the U.S. tax code has a second layer to this problem. The code itself is riddled with provisions that quietly transfer wealth from working families to the federal government during inflationary periods. Tax brackets that don't quite keep up. Capital gains taxed on phantom profits. Thresholds frozen for decades. The cumulative effect is substantial, and it hits mass-affluent households, that is, families earning $150,000 to $500,000, harder than almost anyone else.

These families earn too much to escape the traps and too little to exploit the estate-planning playbook available to the ultra-wealthy. If you are reading this letter, you are probably one of them. So am I.

I want to walk through what I have found in researching this topic, because I think it changes the way we should think about several common financial planning decisions. Especially if you share my view that inflation is likely to run above the Fed's 2% target for a sustained period.

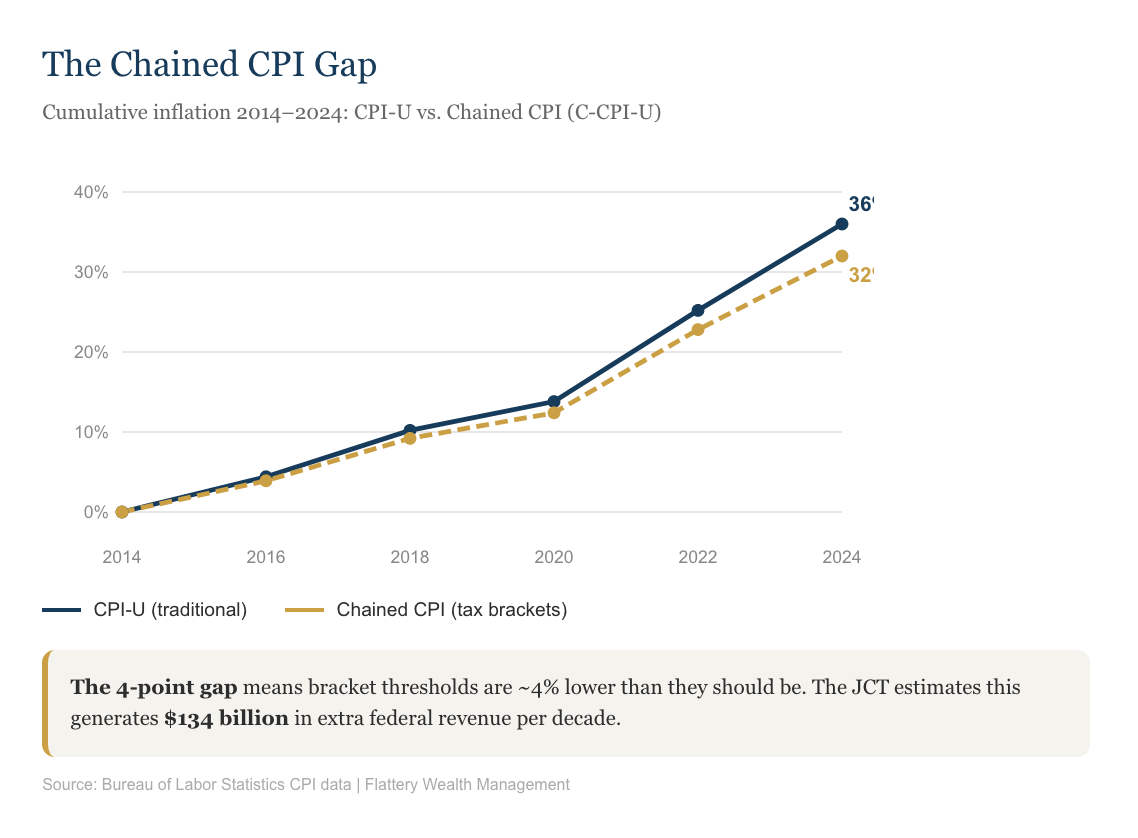

Before 2018, the IRS adjusted tax brackets each year using CPI-U, the standard Consumer Price Index for Urban Consumers. It was imperfect but reasonably straightforward. The Tax Cuts and Jobs Act of 2017 permanently switched to something called the Chained CPI (C-CPI-U), which grows more slowly because it assumes that when prices rise, consumers substitute cheaper alternatives. When beef gets expensive, the index assumes you buy chicken instead.

This is an economist's way of saying your standard of living declined, but don't worry about it.

According to Bureau of Labor Statistics data, the Chained CPI grows roughly 0.2 to 0.3 percentage points slower per year than traditional CPI-U. That does not sound like much. But it compounds. From 2014 through 2024, CPI-U rose approximately 36% while Chained CPI rose approximately 32%. That is a four-point gap in a single decade, and it is permanent.

Here is what that means in practice. The 24% bracket for single filers in 2025 kicks in at $103,350. Under the old CPI-U measure, that threshold would be roughly $105,600, about $2,275 higher. For married couples in the 37% bracket, the threshold sits at $751,600 instead of approximately $768,000. These are not trivial differences. The Joint Committee on Taxation estimated this switch generates $134 billion in additional federal revenue over ten years. That is $134 billion extracted from taxpayers without any visible rate increase, without any vote, through the quiet arithmetic of a different price index.

The Brookings Institution's Hutchins Center has a good explainer on why the chained measure systematically understates the inflation that households actually experience. The Heritage Foundation documented that before bracket indexing even existed (it started in 1985), a 10% inflation rate generated a 17% increase in government revenue. We have come a long way from that era of naked bracket creep, but the new system is still tilted.

And here is the kicker. The switch to Chained CPI was one of the few permanent provisions in the TCJA. Even when the individual rate cuts were scheduled to sunset, this stayed. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, retained it permanently. This mechanism will keep compounding for decades.

One area where Congress has been surprisingly generous is retirement contribution limits. I expected to find that IRA and 401(k) limits had fallen behind inflation. They have not.

The IRA contribution limit was stuck at $2,000 from 1981 through 2001. Twenty years of erosion that cut its real value nearly in half. EGTRRA (2001) finally stepped the limit up aggressively, and it has been climbing since. By 2025, the IRA limit stands at $7,000, a 250% increase from the $2,000 limit in 2000. Cumulative CPI inflation over that same period was approximately 87%. The 401(k) employee deferral limit followed a similar trajectory, rising from $10,500 in 2000 to $23,500 in 2025, a 124% increase.

That said, once CPI indexing actually took hold (2006 for 401(k)s, 2008 for IRAs), the gains have been more modest. The IRS rounds down to the nearest $500, which creates persistent small gaps versus perfect indexing. By 2025, the IRA limit trails perfect CPI indexing from its 2008 base by about 6%, and the 401(k) by about 2%. These gaps are small but real, and they compound over a career.

Here is the scorecard:

The IRA catch-up was frozen at $1,000 for nineteen straight years, during which CPI rose roughly 60%. If indexed from inception, it would be approximately $1,600 today. SECURE Act 2.0 finally addressed this. Beginning in 2026, the IRA catch-up becomes inflation-indexed, rising to $1,100 per the IRS's November 2025 announcement. The SIMPLE IRA catch-up also increases from $3,500 to $4,000. And SECURE 2.0 created the "super catch-up" for 401(k) participants ages 60 to 63, allowing enhanced contributions of up to $11,250, for a total of $34,750 with the base limit. These are genuinely inflation-protective improvements.

For 2026, the IRS announced the 401(k) deferral limit rises to $24,500 and the IRA limit to $7,500, both continuing to outpace underlying inflation.

The implication for planning is straightforward. If you believe future dollars will be worth less (and I do), then the real value of tax-advantaged space is higher than it appears. Every dollar you contribute today to a Roth IRA is a dollar that will never be taxed again, no matter how much the currency depreciates. The contribution limits have outpaced inflation, which means the shelter is getting more valuable in nominal terms.

If the Chained CPI switch is the most consequential stealth tax increase, capital gains taxation is the most consequential distortion in the entire code.

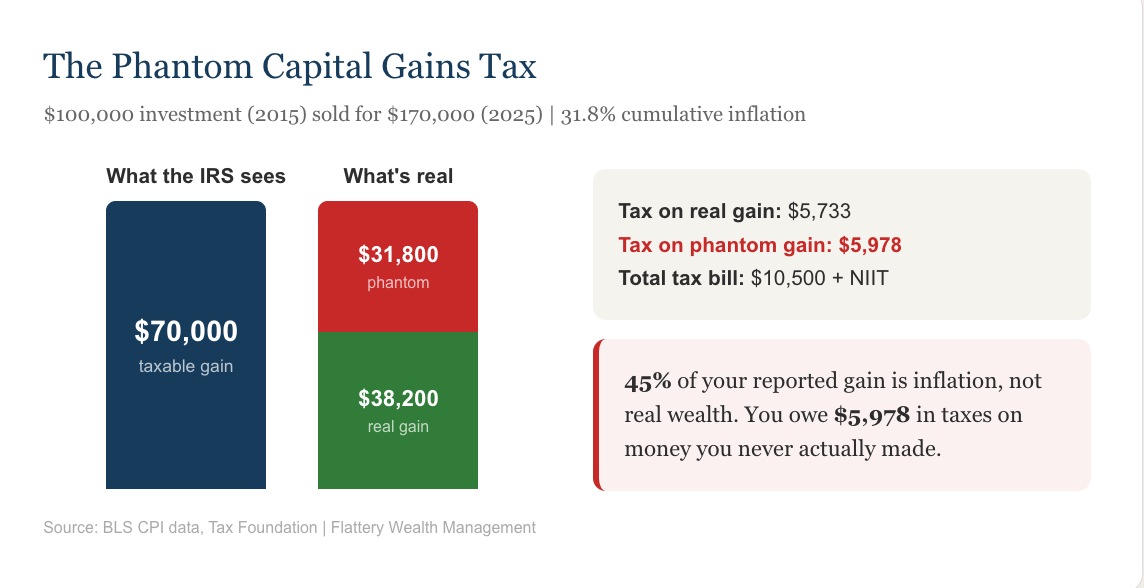

The United States taxes capital gains on nominal values. That is, the raw difference between what you paid and what you sold for, with zero adjustment for the purchasing power lost to inflation during the holding period. The Tax Foundation estimates that approximately one-third of all reported capital gains are purely inflationary, representing no real economic gain whatsoever.

Let me give you a concrete example that hits close to home for many of our clients.

Suppose you purchase an investment for $100,000 in 2015 and sell for $170,000 in 2025. Good trade, right? You made $70,000. Except cumulative inflation over that decade was approximately 31.8% (per BLS CPI data). Your inflation-adjusted cost basis should be $131,800, making your real gain only $38,200. But the IRS does not care about your real gain. It taxes you on the full $70,000.

At a 15% long-term capital gains rate, your tax bill is $10,500. Of that, $4,770 represents tax on the $31,800 in purely phantom inflationary gains, gains that do not exist in real purchasing-power terms. For taxpayers above the NIIT threshold, add 3.8% on that same phantom portion: another $1,208. The total tax attributable solely to inflation reaches $5,978. That is 45% of your total capital gains tax bill, and it is a levy on wealth you never actually accumulated.

This problem only gets worse with longer holding periods and higher inflation. Martin Feldstein's NBER research documented that during the inflationary 1970s, investors could owe capital gains tax on positions that had actually lost real value. His work estimated that the tax-inflation interaction on capital income creates permanent welfare losses equivalent to roughly 1% of GDP annually.

The NIIT makes this worse. The 3.8% Net Investment Income Tax has thresholds ($200,000 single, $250,000 married) that have never been indexed since their creation in 2013. In 2025 dollars, the original $200,000 threshold is equivalent to roughly $262,000. The number of taxpayers subject to NIIT has more than doubled from roughly 3.1 million in 2013 to 7.3 million by 2021, with collections surging from $16.5 billion to $59.8 billion. This is bracket creep in its purest form, not from indexing adjustments, but from a complete absence of any indexing at all.

Despite decades of proposals to index capital gains to inflation (from Reagan through Senator Ted Cruz's Capital Gains Inflation Relief Act of 2025), it has never happened. The OBBBA did not include it. Among OECD countries, only a handful tax real rather than nominal capital gains. The step-up in basis at death provides a complete but posthumous hedge, creating a powerful (and economically distortionary?) incentive to simply never sell.

Not all provisions have moved in the same direction.

The standard deduction represents the greatest legislative generosity. It jumped from $6,350 (single) in 2017 to $12,000 in 2018 under the TCJA, an 89% overnight increase. By 2025, it reached $15,000 for single filers and $30,000 for married couples, with the OBBBA adding a further 5% boost. From a 2000 base of $4,400, that is a 241% increase against roughly 87% cumulative inflation. However, the TCJA simultaneously eliminated the personal exemption ($4,050 per person in 2017), so the net benefit for a single filer was roughly 15% in real terms. Meaningful, but smaller than the headline suggests.

The estate tax exemption has grown astronomically: from $675,000 in 2001 to $13.99 million in 2025, with the OBBBA setting it at $15 million per individual ($30 million per couple) starting 2026, indexed permanently. Fewer than 1,300 estates now owe federal estate tax annually. For the mass-affluent families I work with at Flattery Wealth, the estate tax has essentially been eliminated as a concern.

The AMT tells a similar story. The TCJA's dramatically higher exemptions reduced the affected population from over 5 million taxpayers to roughly 200,000, a 96% reduction.

The gift tax exclusion has roughly tracked inflation, rising from $10,000 in 2000 to $19,000 in 2025 (90% growth versus 87% CPI). Its $1,000-increment rounding creates a staircase pattern that alternately lags and slightly exceeds inflation.

The clear loser is the mortgage interest deduction cap. The original $1 million cap set in 1987 was never indexed. The TCJA reduced it to $750,000 in 2018, and the OBBBA made this permanent, still unindexed. In real terms, the cap has declined by more than 70% since 1987 (when $1 million equaled roughly $2.7 million in 2025 dollars). Meanwhile, itemization rates collapsed from 31% of returns in 2017 to about 9% after 2018, meaning the MID now benefits a much smaller, wealthier group.

For those who do claim it, inflation creates a paradoxical double benefit: higher interest rates generate larger deductible amounts, while inflation simultaneously erodes the real value of fixed-rate mortgage debt. At 4% inflation and a 6.5% mortgage rate in the 24% bracket, the real after-tax borrowing cost falls to approximately 0.9%. That is, for practical purposes, nearly free money in real terms.

If you believe, as I do, that inflation will run structurally above the Fed's 2% target for a sustained period (say 3 to 5%), several tactical moves become more attractive.

Roth conversions become compelling. Converting $100,000 to a Roth and paying $24,000 in taxes today at a 24% rate means that at 4% annual inflation over 20 years, the real cost of that tax payment shrinks to just $10,953 in today's purchasing power. Inflation erodes more than half the real bite. Meanwhile, the converted funds compound tax-free for decades. Morningstar has noted that higher inflation also means wider bracket thresholds each year, creating more room to fill lower brackets with conversion income. The OBBBA making TCJA's lower rates permanent reduces the urgency of "convert before rates rise," but the inflation math still favors paying taxes in today's dollars when you expect tomorrow's dollars to be worth less.

Social Security's frozen thresholds create urgency for pre-retirees. The provisional income thresholds for taxing Social Security benefits ($25,000/$32,000 for 50% taxation and $34,000/$44,000 for 85% taxation) have not been adjusted since 1984 and 1993 respectively. If the $32,000 married threshold had been indexed to wages since 1984, it would be roughly $96,000 today. Originally affecting about 10% of beneficiaries, these frozen thresholds now hit over 50%. The OBBBA's new $6,000 Senior Deduction (ages 65+, phasing out at $75,000/$150,000 MAGI) provides modest, temporary relief through 2028 but does not fix the underlying problem. Pre-retirees should plan Roth conversions specifically to reduce future provisional income and avoid the "tax torpedo," the zone where each additional dollar of income can trigger effective marginal rates exceeding 40% as previously untaxed Social Security benefits become taxable.

Fixed-rate tax-deductible debt becomes a powerful asset. A $500,000 mortgage at 6.5% in the 24% bracket costs 4.94% after the tax deduction. Subtract 4% inflation, and the real after-tax cost is under 1%. At 5% inflation, you achieve a negative real after-tax borrowing rate. You are mathematically paid to borrow. This favors maintaining mortgage debt rather than accelerating payoff, particularly for households who itemize deductions.

I want to briefly note what recent legislation has and has not accomplished on this front.

The Inflation Reduction Act of 2022 was primarily a climate and energy law. Its tax provisions (a 15% corporate alternative minimum tax, a 1% stock buyback excise tax, and roughly $260 billion in clean energy credits) did nothing to address bracket creep, capital gains indexing, frozen thresholds, or any other inflation-tax distortion. The corporate AMT threshold itself is not indexed to inflation. The Tax Foundation estimated the law would reduce long-run GDP by approximately 0.2%. The name was, by any honest assessment, a misnomer.

SECURE Act 2.0 delivered some helpful inflation-related improvements: indexing the IRA catch-up (rising to $1,100 in 2026), creating the super catch-up for ages 60 to 63, raising the RMD age to 73 (and 75 by 2033), and requiring high earners ($145,000+ in FICA wages) to make catch-up contributions on a Roth basis starting 2026, which in an inflationary environment actually benefits those workers by channeling contributions into the tax-free growth vehicle.

The OBBBA was the most consequential legislation, making TCJA's individual rate structure permanent, setting the estate tax exemption at $15 million (indexed), and restoring 100% bonus depreciation, which partially addresses inflation's erosion of depreciation allowances by front-loading deductions into years when dollars are worth the most. But it preserved Chained CPI permanently, made the unindexed $750,000 mortgage cap permanent, and did not address Social Security taxation thresholds or capital gains indexing.

Across nearly every margin of the tax code, higher inflation transfers wealth from taxpayers to the Treasury.

Chained CPI underadjustment generates roughly $13 billion annually in extra revenue compared to CPI-U indexing (based on the JCT's ten-year estimate). Taxation of nominal capital gains produces an estimated $10 to $34 billion per year in taxes on purely inflationary gains (per Tax Foundation analysis). Frozen thresholds (Social Security taxation since 1984, NIIT since 2013, the Additional Medicare Tax since 2013, the home sale exclusion since 1997) collectively pull millions of additional taxpayers into taxes never designed to reach them. And each percentage point of unexpected inflation reduces the real burden of roughly $36 trillion in outstanding federal debt by approximately $180 billion.

The offsetting costs to the government are real but smaller. Social Security benefits are indexed to CPI-W, requiring larger nominal outlays. Higher interest rates on new debt issuance increase borrowing costs. And since September 2022, the Federal Reserve has been operating at a loss, eliminating the seigniorage remittances that previously sent $100+ billion annually to the Treasury.

On balance, the government wins. Martin Feldstein's NBER research remains the definitive framework: the interaction of inflation with nominal taxation of interest, capital gains, and depreciation creates permanent economic distortions that reduce welfare by roughly 1% of GDP annually, a cost borne entirely by the private sector while the Treasury collects the revenue windfall.

As an Austrian sympathizer who has watched the dollar's purchasing power decline over my career, I find none of this surprising. But I think putting specific numbers to it is useful. The inflation tax is not just a metaphor. It is embedded in the code, line by line, threshold by threshold.

The tax code is tilted against you in an inflationary world. But knowing where the tilts are is the first step toward leaning into them.

The switch to Chained CPI is the most consequential stealth tax increase of the past decade. Capital gains taxation without inflation adjustment is the single largest distortion in the code. Frozen thresholds on everything from Social Security taxation to the NIIT are dragging millions into taxes that were never designed for them.

But the planning opportunities are out there. Roth conversions exploit inflation's erosion of today's tax payment. Fixed-rate deductible debt generates negative real after-tax borrowing costs at elevated inflation. And aggressive use of retirement contribution limits, which have meaningfully outpaced inflation, remains the single most powerful tax shelter available to working households.

---

Tax bracket and threshold data:

Chained CPI and indexing:

Capital gains and inflation:

Retirement contribution limits:

TCJA, OBBBA, and legislative context:

---

Flattery Wealth Management, LLC is a registered investment advisor offering advisory services in the States of Missouri, Kansas, and other jurisdictions where exempt from registration. This communication is provided for informational purposes only and should not be construed as investment, tax, or legal advice. It does not constitute an offer, solicitation, or recommendation to buy or sell any specific security or instrument. Consult a qualified tax professional before making decisions based on this information. There is no assurance that any strategy discussed will be successful or that historical trends will continue.

-modified.png)

Andrew Flattery is a CERTIFIED FINANCIAL PLANNER™ and Principal of Flattery Wealth Management. He serves affluent families in Kansas City and nationwide. Flattery is the host of Gentleman Speculator, a podcast on legacy, investing, and the life well-lived. When he’s not helping individuals build wealth, you can catch him playing rec sports, writing children's books, and spending time with his wife and four children.